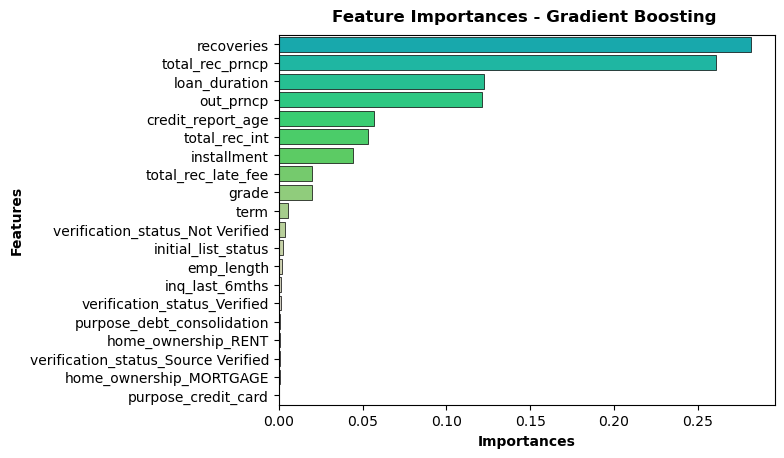

In the ever-evolving landscape of finance, the ability to effectively manage credit risk is paramount for ensuring the stability and profitability of lending institutions. Leveraging machine learning techniques presents a promising avenue to enhance credit risk analysis and prediction. This case study delves into our journey of utilizing advanced analytics to tackle credit risk, outlining the challenges faced and strategies implemented to overcome them.

We created a system where the tool automatically decides to buy or sell stocks based on news articles. If the news suggests a stock will go up, it might decide to buy (long). If the news suggests a stock will go down, it might decide to sell (short). If the news isn’t clear, it might choose to do nothing (preserve). We make sure to close the deals the day after the next trading day to stay flexible.

To control how much we buy or sell, we use a special formula based on recent returns and how likely the news is to be accurate. We also calculate a pretend return rate for when we choose to do nothing.

The percentage of good loans surged by 11.26%, soaring to an impressive 98.8%. Concurrently, the incidence of bad loans witnessed a remarkable decline of 89.29%, plummeting to a mere 1.2%. These outcomes underscored the significant efficacy of the model in mitigating credit risk, affirming its potential to revolutionize lending practices and bolster financial stability.

Despite the myriad challenges encountered, our journey of leveraging machine learning for credit risk analysis has been a transformative one. By embracing innovation, overcoming obstacles, and adopting a holistic approach, we have enhanced our ability to assess and mitigate credit risk effectively. Moving forward, we remain committed to harnessing the power of data-driven insights to drive sustainable growth and resilience in our lending practices.

Turn Your Startup into

Success Story!

Join Us to remain update

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}